The United States foodservice industry witnessed a significant divergence in the performance of plant-based alternatives in 2025, with non-dairy milk and creamers experiencing robust growth, while plant-based protein sales, including meat analogues, continued to decline. This trend, detailed in a new analysis by the Good Food Institute (GFI), highlights a complex and evolving consumer landscape, where dairy alternatives are gaining traction in a crucial sector of the food market, even as the broader plant-based protein category grapples with challenges.

According to the GFI report, which analyzes U.S. foodservice market insights from 2021 to 2025, dollar sales of non-dairy milk surged by 16% in U.S. foodservice establishments last year. This growth rate outpaced that of conventional cow’s milk, indicating a substantial shift in consumer preferences within coffee shops, restaurants, and non-commercial food outlets. Plant-based creamers also demonstrated positive momentum, with a 4% increase in dollar sales in 2025. Both product segments have now secured a double-digit share of their respective categories by volume, signaling their established presence and growing appeal.

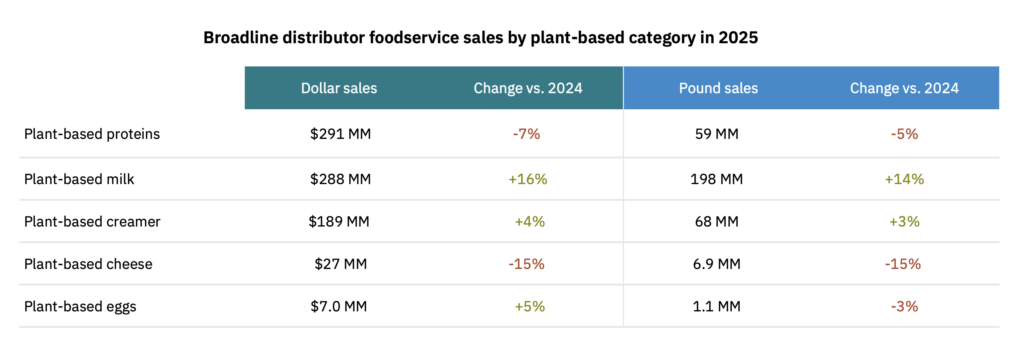

In stark contrast, sales of plant-based proteins, a category encompassing meat alternatives, tofu, tempeh, and whole-food formats like veggie burgers, experienced a contraction. The report indicates a 7% decrease in dollar sales for this segment, marking a continuation of a downward trend observed since its peak in the post-pandemic year of 2022. This decline occurs even as the price differential between plant-based proteins and conventional meat has narrowed, suggesting that factors beyond price are influencing consumer purchasing decisions in this area.

The Good Food Institute emphasized the role that foodservice operators can play in revitalizing the plant-based protein market. Strategies such as innovative menu presentations, creative preparation of plant-based ingredients in professionally crafted dishes, and increased availability can significantly drive consumer awareness and engagement. Furthermore, these operators serve as critical channels for new product launches and valuable feedback loops, which are essential for product development and market refinement.

Dairy Alternatives Flourish While Cheese Trails

The performance of dairy alternatives in the U.S. foodservice sector paints a picture of dynamic growth for milk and creamers, contrasting with a less favorable environment for plant-based cheese. Non-dairy milk saw a notable 14% increase in pound sales, significantly outperforming conventional milk’s 4% rise. This surge propelled the dollar sales of plant-based milk to $288 million in foodservice, marking five consecutive years of consecutive growth. Consequently, these alternatives now command a 13% share of total milk pound sales, a testament to their increasing integration into consumer diets.

Similarly, dairy-free creamers achieved $189 million in dollar sales within the U.S. foodservice landscape, with pound sales rising by 3%. Plant-based creamers hold the most substantial market share among all analyzed plant-based categories in this channel, representing 28% of all creamer sales. The GFI report suggests that the removal of plant-based surcharges by coffee chains likely contributed to this positive trend. Offering plant-based options as the default choice and eliminating additional fees have been identified as effective strategies for boosting sales.

However, the success story of dairy alternatives does not extend to vegan cheese. This category experienced a considerable downturn, with both dollar and pound sales declining by 15% in 2025. This decline occurred against a backdrop of flat pound sales for conventional dairy cheese, indicating a broader challenge for plant-based cheese in foodservice environments.

Another segment within dairy alternatives, plant-based eggs, represented the smallest category analyzed, generating only $7 million in dollar sales. Despite a 5% uptick in dollar sales, pound sales saw a 3% decline. The GFI report attributes the leveling off of usage, despite potential benefits from volatility in the conventional egg market due to avian influenza outbreaks, to increasing prices for plant-based eggs, which surpassed six dollars per pound in 2025. This price sensitivity underscores the ongoing consumer scrutiny of value propositions in the plant-based market.

Plant-Based Proteins Face Headwinds Despite Narrowing Price Gap

The broader plant-based protein segment, which includes meat alternatives, tofu, tempeh, and whole-food options, recorded $291 million in dollar sales in the U.S. foodservice sector last year. However, this figure masks a 5% decline in pound sales, a stark contrast to the 2% increase observed in conventional meat sales. As a result, vegan proteins continue to represent a modest 0.4% share of the overall meat category within foodservice.

Within the plant-based protein segment, meat alternatives constitute the largest portion, accounting for 54% of all sales. Among these, beef-style alternatives lead with a 59% share, followed by chicken alternatives at 22% and pork alternatives at 19%. In terms of product formats, burger patties remain the most popular offering, representing 38% of sales within the plant-based meat sub-category.

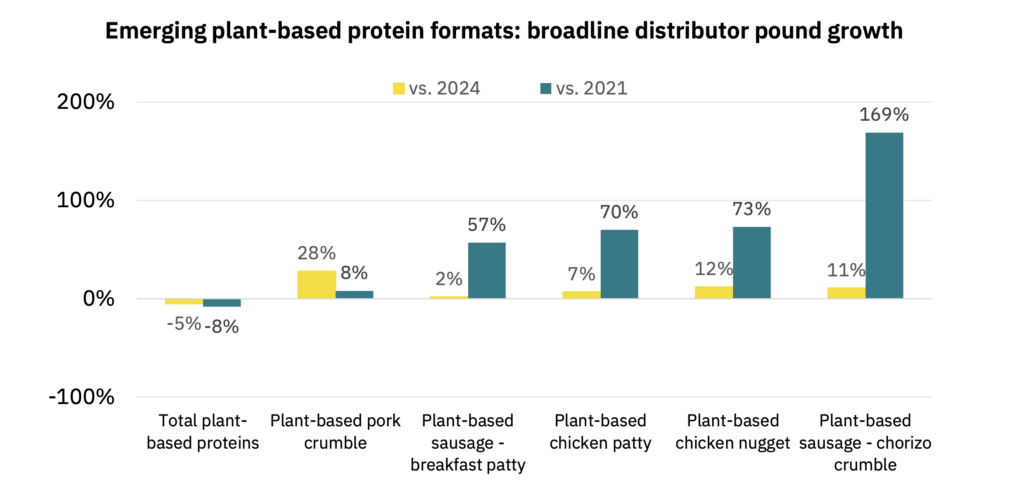

Despite the overall decline, certain sub-categories within plant-based proteins demonstrated resilience and even growth. Plant-based pork alternatives saw a 3% increase in dollar sales, a positive outlier when compared to the 16% and 6% declines experienced by beef and chicken alternatives, respectively. Specific formats that performed particularly well included pork crumbles (up 28% from 2024), chicken nuggets (up 12%), chorizo crumbles (up 11%), and chicken patties (up 7%). These niche successes suggest that innovation and targeted product development can still yield positive results.

While restaurants remain the primary buyers of plant-based proteins, their purchases saw a significant decline of 15%. A concerning statistic from the report indicates that 85% of restaurants do not offer any plant-based dishes on their menus, a potential barrier to increased adoption. In contrast, sales to non-commercial foodservice outlets, including those in educational institutions, healthcare facilities, business and industry settings, and government operations, showed an upward trend, suggesting a different set of drivers and consumer demands in these environments. Tofu and tempeh, which together account for 36% of plant protein sales in U.S. foodservice, experienced flat performance. Whole-food products, such as those made from vegetables, grains, and nuts, constitute another 9% of the market and saw a 6% growth in pound sales, indicating a continued consumer interest in less processed, whole-ingredient plant-based options.

Price Premiums Persist, But The Gap Is Closing

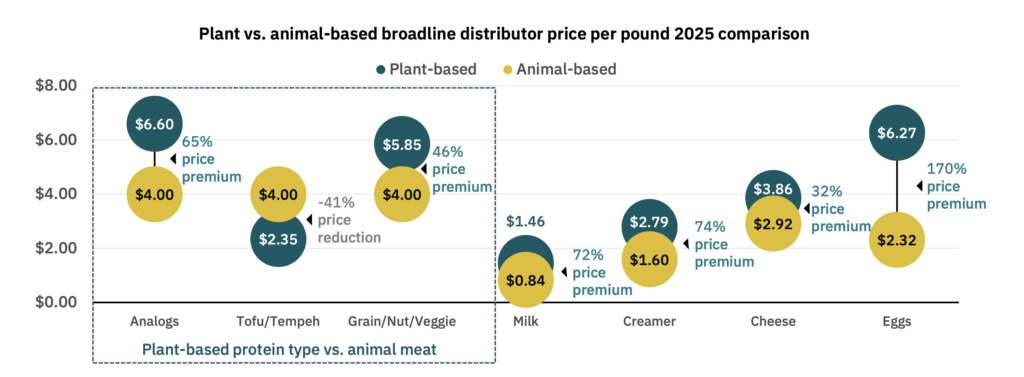

The price premium associated with plant-based foods remained a significant factor in consumer decision-making throughout 2025. Meat and milk alternatives continued to be priced approximately 60-70% higher than their conventional counterparts in the foodservice sector. However, the price gap for plant-based proteins has seen a slight reduction, largely influenced by the rising costs of conventional meat products.

Currently, plant-based meat is priced at a 65% premium compared to conventional meat, while alternatives like veggie burgers are 46% more expensive. Milk alternatives carry a substantial 72% premium, and plant-based eggs exhibit the largest price gap, at a staggering 170% premium over conventional eggs. This significant difference in pricing for eggs is a notable barrier to widespread adoption.

In a notable exception, tofu and tempeh stand out as the only plant-based protein categories that are cheaper than conventional meat, offering a price advantage of 41% relative to animal protein. This cost-effectiveness could position them favorably for consumers seeking budget-friendly plant-based options.

The GFI report also highlighted shifts in price dynamics over the past year. While plant proteins have become 1% cheaper, the cost of animal meat has risen by 4%. For milk and non-dairy alternatives, prices increased by 2% for both. Vegan eggs saw an 8% price increase, while conventional eggs experienced a more significant 15% rise. These fluctuating price points underscore the dynamic nature of the food market and the impact of external factors such as supply chain disruptions and inflation.

The persistent price gap, despite its gradual narrowing, has tangible implications for the foodservice industry. Consumers who purchase plant-based meat alternatives in restaurant chains tend to make nearly 50% more purchases and spend over $500 more per dining-out visit compared to the general population. Furthermore, the inclusion of a meat alternative dish on a check increases the average party total by $2, presenting a potential revenue opportunity for restaurants that strategically incorporate these options.

Taste and Affordability Remain Key Drivers for Consumer Adoption

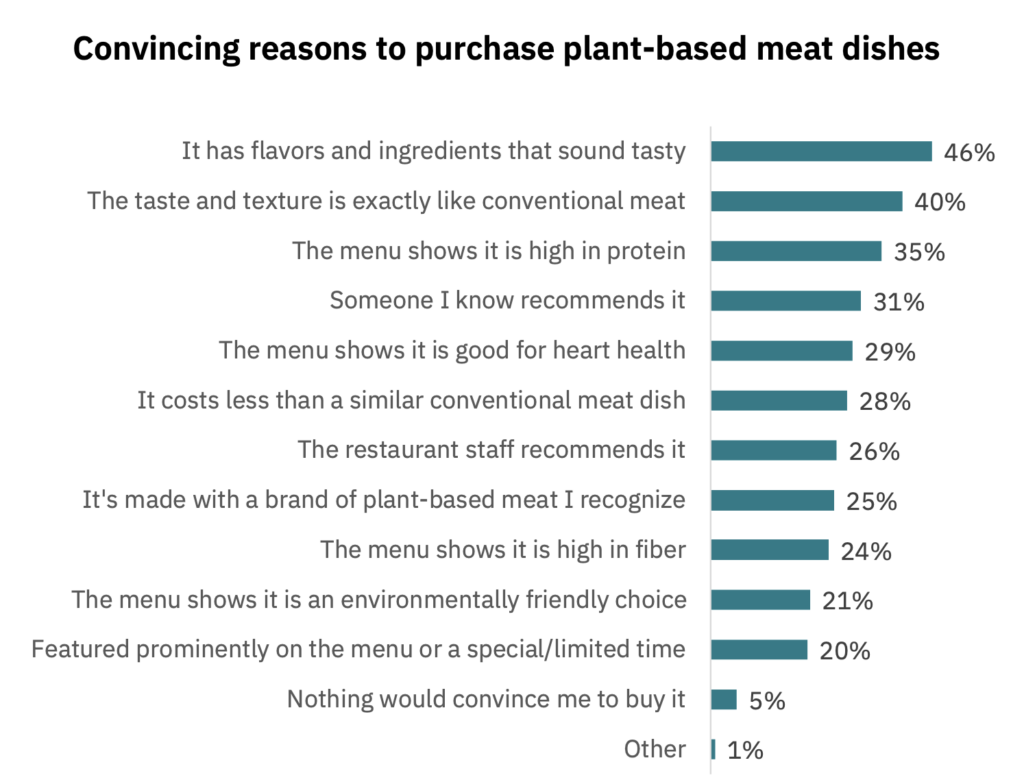

Consumer research consistently identifies taste and affordability as the two most compelling factors influencing the adoption of plant-based foods in the United States, and these preferences extend significantly into the foodservice sector. A comprehensive survey conducted by GFI and Morning Consult in December, involving 3,500 individuals, revealed that only 7.3% of diners purchased plant-based meat in the past year, with a substantial 62% of those purchases being a one-time occurrence.

A significant barrier to increased consumption is the lack of availability. Thirty-five percent of Americans reported not ordering meat alternatives at a restaurant due to their absence from the menu. When asked about what would encourage them to purchase more plant-based meat products, 46% of respondents cited the need for delicious flavors and ingredients. An additional 40% emphasized that the taste and texture must closely replicate that of conventional meat. For 35% of consumers, the menu should clearly indicate that a plant-based meat dish is a high-protein option.

The survey also underscored the influence of social proof and perceived health benefits. Thirty-one percent of individuals expressed openness to trying meat alternatives if recommended by someone, while 29% would be more inclined if the menu highlighted the heart-healthy attributes of the dish. Cost remains a critical consideration, with 28% of consumers stating they would purchase plant-based meat if it were less expensive than a conventional meat dish.

Encouragingly for the plant-based industry, only a small fraction of Americans, approximately 5%, indicated that nothing could convince them to purchase plant-based meat in a restaurant or foodservice setting. This suggests a substantial market segment that remains open to persuasion.

The Good Food Institute concluded that improvements in both the taste and price of plant-based meat dishes are crucial for motivating diners to choose them more frequently. Additionally, employing strategies such as highlighting health benefits and leveraging personal recommendations can further enhance consumer appeal and drive broader adoption within the competitive foodservice landscape. The findings suggest that while progress is being made, particularly in dairy alternatives, the plant-based protein sector requires targeted innovation and strategic market positioning to overcome current challenges and capitalize on its growth potential.