The global demand for protein continues its relentless upward trajectory, and a significant shift in consumer preference is set to redefine food markets worldwide. New analysis indicates that by 2030, the volume sales of legumes, encompassing beans and pulses, are predicted to surpass those of meat in nearly every region across the globe. This burgeoning demand for plant-based protein sources is driven by a confluence of factors, including rising meat prices, growing health consciousness, and an increasing awareness of the environmental implications of traditional protein consumption.

For the past few years, legumes have occupied a prominent position in food discourse. Consumers, keenly aware of the need to maximize protein and fiber intake for optimal health, have increasingly turned to these versatile and nutrient-dense foods. Simultaneously, the meat industry has been grappling with significant supply chain disruptions. The escalating climate crisis, manifesting in extreme weather events that impact livestock and crop yields, coupled with ongoing geopolitical tensions that disrupt global trade and agricultural inputs, has led to a dramatic surge in meat prices. This economic pressure has made legumes a far more accessible and attractive protein alternative for a growing number of consumers in numerous countries.

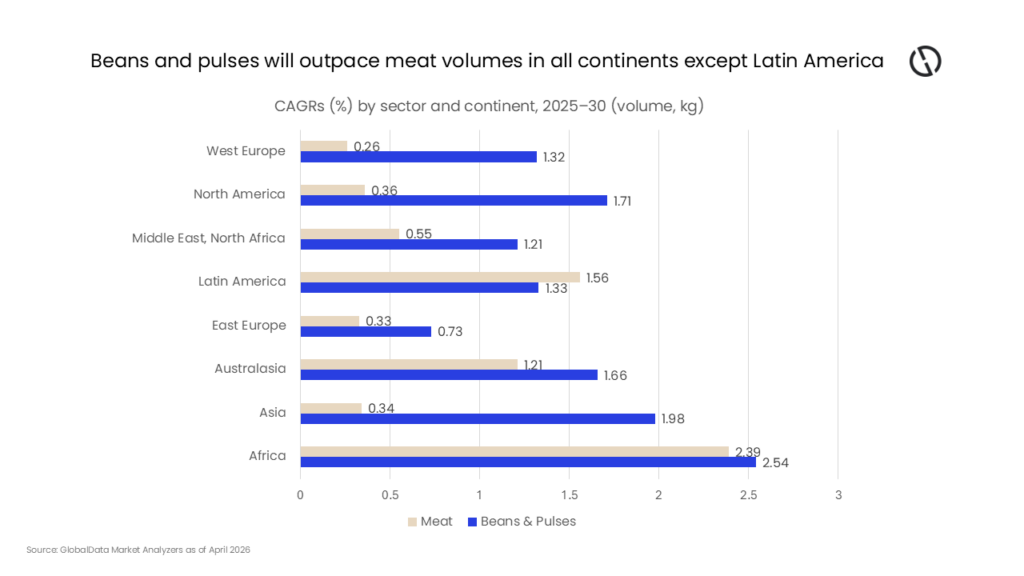

This projected market transformation is substantiated by recent comprehensive analysis from GlobalData, a leading data analytics firm. Their findings suggest that legumes are on an ascendant path, with global volume sales of beans and pulses forecasted to expand at a compound annual growth rate (CAGR) of 1.7% through 2030. This growth rate significantly outpaces that of meat volumes, which are projected to grow at a more modest CAGR of 0.7%. This trend is remarkably consistent across virtually all geographical regions, with the sole exception being Latin America. This widespread adoption underscores a powerful global movement towards plant-based protein, even in regions where the meat sector currently holds a larger market share.

Asia: The Epicenter of the Legume Renaissance

The sustained global appetite for protein is a key driver behind this legume revolution. GlobalData’s Q1 2026 consumer survey revealed that a substantial 50% of respondents intend to maintain their current protein intake levels over the next twelve months, while an additional 36% plan to increase their consumption. This data builds upon previous findings; a survey conducted a year prior indicated that 32% of respondents considered protein content a crucial factor when evaluating the healthfulness of a product.

"Consumers are keenly interested in protein and recognize its significant health benefits," stated Eve Forshaw, a consumer analyst at GlobalData. This consumer interest is increasingly being bolstered by official dietary recommendations. The American Heart Association’s (AHA) latest dietary guidelines, for instance, highlight nine essential elements for a heart-healthy diet. Among these, a notable emphasis is placed on transitioning to healthier protein sources, specifically advocating for the substitution of meat with plant-based alternatives such as legumes, nuts, and seeds.

Forshaw further commented, "The AHA’s advice aligns seamlessly with the emerging trend of ‘Zebra consumption,’ a dietary pattern where individuals alternate between meat-based and plant-based proteins to achieve a more balanced nutritional profile." This strategic dietary diversification not only addresses health concerns but also acknowledges the growing environmental awareness among consumers.

Regional Dynamics: A Shifting Protein Landscape

The projected growth of the legume market is expected to be most pronounced in Asia. While Africa is also anticipated to witness significant growth in legume consumption, with volumes expanding at a CAGR of 2.54% – closely mirroring the projected 2.39% rise in meat consumption on the continent – Asia presents the most striking divergence. In Asian markets, meat sales are only expected to increase by a marginal 0.34%. In stark contrast, beans and lentils are set to experience a substantial hike of 1.98%, a growth rate nearly six times higher than that of meat.

This trend is not confined to Asia. The CAGRs for these plant-based proteins are also considerably higher than for meat in other major markets: North America (1.71%), Australasia (1.66%), and Western Europe (1.32%). The only exception to this global pattern is Latin America, where GlobalData estimates a 1.33% CAGR for beans and lentils, but a higher 1.56% growth rate for meat. This regional anomaly may be attributed to deeply ingrained culinary traditions and the current economic accessibility of meat in some Latin American countries.

The expanding interest in traditional plant-based proteins is occurring even as consumer awareness regarding specific plant protein sources remains somewhat fragmented. GlobalData’s 2025 survey indicated that while only 7% of consumers were unfamiliar with chicken and meat, this figure rose significantly for plant-based alternatives: 13% for soy protein, 21% for pea protein, and a notable 38% for hemp protein. Despite this disparity in familiarity, the underlying trend is clear. "Despite lower familiarity with specific plant protein sources, there is a growing appetite for protein-rich plant-based foods," Forshaw observed. This suggests that as consumers encounter these ingredients more frequently in their diets and through marketing efforts, awareness and acceptance are likely to increase.

Mung Beans: A Rising Star in the Plant-Based Arena

Within the diverse world of legumes, GlobalData’s analysis identifies mung beans as a particularly promising area for innovation for food manufacturers seeking "meat-comparable" alternatives. Mung beans boast a high protein content, offering approximately 27 grams per 100 grams, a figure that aligns closely with that of chicken and red meats. Furthermore, their versatility allows them to be incorporated into a vast array of dishes.

Historically, mung beans have been a staple food for thousands of years across the Indian subcontinent and Southeast Asia. They form the foundation of numerous traditional dishes, including dal (lentil stew), breakfast crepes, and various soups. Revered for their affordability, mung beans are also a rich source of antioxidants and dietary fiber, and crucially, they contain all nine essential amino acids, making them a complete protein source.

The functional properties of mung beans are now being leveraged by innovative food technology startups. Companies are isolating mung bean protein to create plant-based alternatives that mimic the taste, texture, and culinary functionality of animal products. A prime example is Eat Just, a California-based company that uses mung bean protein to produce its popular liquid egg substitute, Just Egg. This product replicates the structure and texture of scrambled eggs and possesses the same gelation, thickening, binding, and emulsification properties required for various culinary applications.

"Mung beans stand out as a commercially attractive offering," Forshaw explained. "They deliver meat-comparable protein levels in whole-food forms while also possessing functional properties like gelation, emulsification, and binding in their protein isolate form." This dual role, as both a pantry staple and a versatile ingredient for plant-based innovations, positions mung beans as a strategic opportunity for manufacturers and investors looking to capitalize on the next wave of plant-based protein growth.

The Inflationary Tailwind: Economic Pressures Fueling Legume Demand

The burgeoning interest in legumes is also being significantly amplified by broader economic trends, particularly global inflation. This phenomenon is increasingly influencing national dietary recommendations and consumer purchasing decisions. In the Netherlands and Finland, for instance, updated food-based dietary guidelines are actively encouraging a shift away from meat consumption towards beans.

In the United Kingdom, health experts are actively campaigning for governmental and corporate support to enhance the appeal of beans and whole plant foods. In 2024, meals predominantly featuring vegetables, beans, and legumes saw the most substantial net increase (46%) within the entire plant-based food category. The Food Foundation, a prominent advocacy group, has emphasized the need for a strategic reallocation of promotional spending towards nutritious plant foods. Their recommendations advocate for advertising and promotional strategies that specifically highlight beans as the most affordable, sustainable, and healthiest plant-based alternatives to meat, noting that their consumption is not dictated by income levels.

This economic advantage of legumes over meat has become even more pronounced. Since 2020, the average cost of meat in British supermarkets has risen at a rate over six times faster than that of shelf-stable beans. This stark price disparity, coupled with the growing consumer preference for "veg-led" foods rich in protein and fiber, has contributed to a resurgence in the vegan food market in the UK. According to Tesco, a major UK retailer, vegan food sales have seen growth for the first time in several years.

Bethan Jones, plant-based food buyer at Tesco, commented on this shift, stating, "A growing micro-trend focused on whole-food plant proteins – including beans, lentils, chickpeas, tofu, and wholegrains – is helping to drive renewed sales, signaling a shift from short-term trend to lasting dietary change." This suggests that the current momentum behind legumes is not merely a fleeting fad but indicative of a fundamental and enduring transformation in dietary habits. The convergence of health consciousness, environmental concerns, and economic realities is firmly positioning legumes as a cornerstone of future global protein consumption.