China is in "year zero" of a profound food systems transition, with the government elevating alternative proteins to a strategic priority in its ambitious bid to transform into a major global food exporter. This assertion comes from a comprehensive new analysis by Systemiq and the Gordon and Betty Moore Foundation, which meticulously charts the East Asian nation’s path toward leadership in the alternative protein sector by 2050. The report draws compelling parallels to China’s successful strategies in green energy and mobility, suggesting a playbook for industrial transformation is being rigorously applied to the future of food.

The genesis of this shift can be traced to dramatic demographic and economic changes over the past four decades. Between 1978 and 2020, China’s population surged by an estimated 450 million, while per capita income expanded by an astonishing 25-fold. This economic prosperity catalyzed a significant dietary evolution, moving away from traditional staples like starchy roots and pulses towards a greater consumption of animal proteins, processed foods, and convenience products. Consequently, animal protein intake saw a tenfold increase during this period, with meat, dairy, fats, and sugars driving the overall rise in per-capita food consumption. However, this dietary evolution came at a significant environmental cost. The production of animal-based foods requires substantially more land, water, and feed compared to plant-based alternatives. The report underscores that this surge in consumption has consequently "tightened the link between diets, environmental stress, and food security."

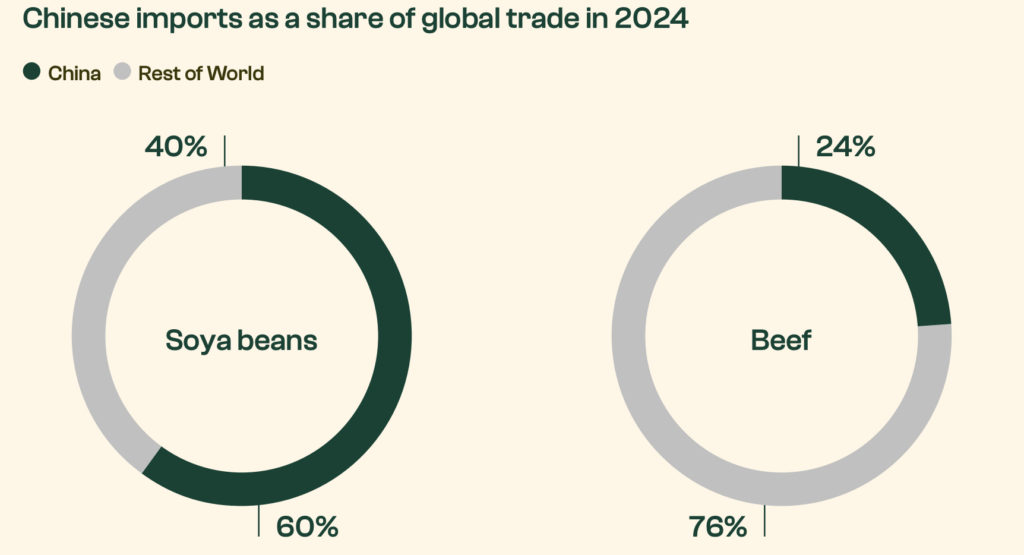

For the last two decades, China has been a central force in global agricultural demand, establishing itself as the world’s largest agricultural importer. This reliance has resulted in a substantial trade deficit, estimated at $124.5 billion. The nation’s import dependency is particularly pronounced in key commodities, accounting for 60% of global soy imports and a significant 24% of beef imports. However, a confluence of factors—including the increasing frequency of climate shocks, escalating geopolitical tensions, and the volatility of international trade disputes—has prompted China’s policymakers to re-evaluate its food security strategy. Recognizing the vulnerabilities inherent in its import-dependent model, food sovereignty has been elevated to a core pillar of national security. Systemiq’s projections indicate a pivotal shift: demand for animal protein is expected to plateau around 2030 before embarking on a sustained decline through 2050 and beyond. This anticipated contraction in global demand has profound implications for the international protein landscape.

Tapping the Green Energy and EV Playbook: A Strategy for Food System Transformation

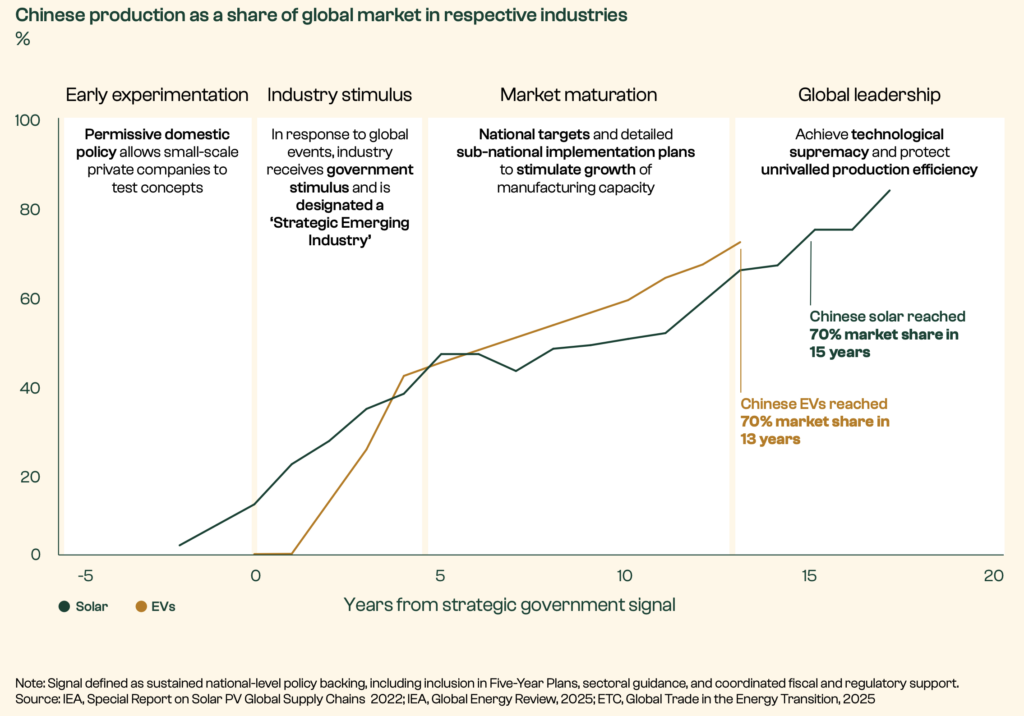

The report highlights that early indicators suggest China is leveraging the same industrial strategy that propelled it to undisputed leadership in the green energy and mobility sectors. Over the past decade, global solar energy capacity has surged by more than 30-fold, while electric vehicle (EV) sales have experienced a remarkable 50-fold increase, now representing 7% and 20% of global electricity and vehicle usage, respectively. China has been the primary catalyst for both these transitions, rapidly ascending from minimal production to dominating 70% of global solar energy and EV manufacturing within a mere 15 years. This rapid ascent is a testament to the efficacy of its strategic approach and its capacity for decisive action in response to global signals.

Chinese policymakers strategically integrated solar power into national industrial plans, mobilizing export incentives and concessional financing to build manufacturing capacity well ahead of domestic demand. As global deployment accelerated, costs plummeted, and economies of scale were achieved, transforming China from a marginal producer into the world’s preeminent solar manufacturer. A similar trajectory was observed in the electric vehicle sector. In both these sectors, incumbent systems—fossil fuels for energy and internal combustion engines for mobility—continued to operate but could no longer be optimized to overcome their inherent limitations. Simultaneously, alternative technologies, though commercially immature, already existed. Their success hinged on the strategic alignment of ambitious targets, robust capital investment, supportive regulatory frameworks, and extensive manufacturing capabilities.

While acknowledging the fundamental differences between agriculture and the energy and mobility sectors, Systemiq emphasizes the value of drawing parallels. The food system is inherently more complex, influenced by biological and physical constraints, deeply embedded in cultural practices, and subject to greater political sensitivity than other industries. Consequently, substitution within the food system presents a more intricate challenge. Nevertheless, the report argues that these differences do not preclude large-scale, transformative change. In the cases of solar power and EVs, the objective was to achieve technological leadership and reduce reliance on fossil fuels. Similarly, in the realm of food, China aims to enhance self-sufficiency and cultivate expertise in future-oriented innovations.

The Chinese government’s recognition of this imperative is evident in its national planning documents. Food security was explicitly placed alongside energy and finance as a critical national priority in the 14th Five-Year Plan (2021-2025). The subsequent plan, covering the period up to 2026, deepens this focus, with specific emphasis on food security, agricultural modernization, protein diversification, and the development of novel food technologies. This strategic prioritization signals a clear intent to reshape the nation’s food landscape.

China’s Future Food Playbook: A Five-Pillar Strategy for Transformation

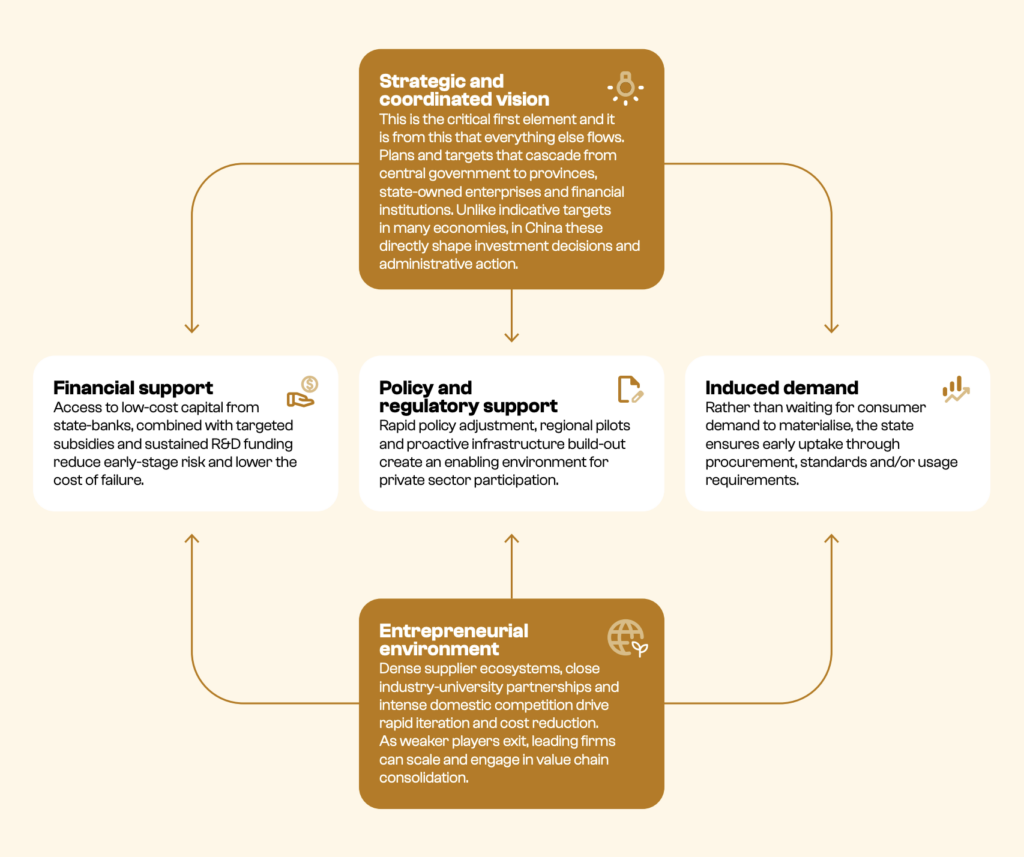

The government’s proactive embrace of alternative proteins signifies that China is currently at "year zero" of its food system transformation. Systemiq has outlined a strategic playbook comprising five mutually reinforcing mechanisms that are driving this ambitious shift:

-

Strategic and Coordinated Vision: This foundational element involves a clear, top-down vision articulated through national five-year plans. These plans cascade from the central government to provincial authorities, state-owned enterprises, and financial institutions. The targets set within these plans directly influence investment decisions, administrative actions, and crucially, signal government intent to the market. This coordinated approach ensures alignment across various sectors and stakeholders.

-

Entrepreneurial Ecosystem: A key driver is the fostering of a dynamic entrepreneurial environment characterized by dense supplier ecosystems, robust industry-university partnerships, and intense competition. This environment encourages rapid iteration, innovation, and cost reduction. Once a sector is prioritized, entry barriers are lowered, and competition is actively encouraged. As less competitive players exit the market, leading firms gain the opportunity to scale up and engage in value-chain consolidation, further strengthening the sector.

-

Financial Support: The availability of substantial financial backing is critical. Low-cost capital from state-owned banks, targeted subsidies, and sustained research and development (R&D) funding serve to de-risk early-stage ventures and reduce the cost of failure. This financial infrastructure enables companies to invest at scale even before full commercial viability is established, thereby accelerating learning curves and facilitating rapid expansion. This mirrors the financial mechanisms employed in the successful green energy transition.

-

Policy and Regulatory Support: Effective policy and regulatory frameworks are equally vital tools. Clear political signaling from the government reduces long-term uncertainties for investors and businesses. Furthermore, China’s demonstrated ability to rapidly amend regulations in response to global developments allows policy to evolve in tandem with technological advancements. Proactive infrastructure build-out creates the necessary physical and institutional landscape for new industries to scale efficiently.

-

Inducing Consumer Demand: Instead of passively waiting for consumer demand to materialize, China actively seeks to stimulate it. This is achieved through early uptake initiatives, including procurement programs and the establishment of usage standards. These measures provide firms with the certainty required to invest in novel technologies and help accelerate learning and cost reduction processes. The implementation of mandates, quotas, and fleet or deployment targets actively creates markets for these emerging technologies, ensuring a foundational customer base.

The Three Phases of China’s Protein Transition: A Projected Timeline

Following this "year zero" phase, the report envisions how this strategic playbook will unfold over the coming decades, positioning China as a major food exporter and a global leader in the alternative protein ecosystem.

2030: Optimization and Incremental Change

By the end of the decade, daily food consumption patterns are expected to remain largely similar to current trends, with demand for animal protein showing little significant change. However, China’s concerted efforts to reduce import dependencies will likely lead to a substantial 25% reduction in soybean imports. Alternative proteins are predicted to remain a niche segment of the market, having not yet significantly altered consumer habits or markedly reduced meat and dairy consumption, largely due to their still-higher price points. Despite this, consistent strategic signaling from China’s leadership will continue to fuel industry innovation. As experience and scale expand, costs will gradually decrease, prompting businesses across the retail and foodservice sectors to experiment more widely with alternative protein offerings. Fermentation-derived ingredients are projected to reach price parity with their animal-based counterparts by 2028. Plant-based alternatives are expected to capture a significant 19% share of the overall dairy market by this year.

2040: Kickstarting Structural Disruption

The period leading up to 2040 is anticipated to witness the commencement of structural change within the food system. As plant-based and fermentation-derived proteins scale from pilot projects to commercial deployment, they are expected to disrupt the most expensive animal protein categories first. These alternatives will achieve price parity with beef and high-value seafood, capturing approximately 14% and 16% of these respective markets. Concurrently, the adoption of genetically modified and engineered crops will continue to enhance yields for maize and soy, leading to a projected 30% reduction in their imports compared to 2025 levels. Fermentation of maize can significantly boost its native protein content, positioning it as a viable substitute for soy and a crucial feedstock for alternative protein production. Notably, by 2040, China is projected to become a net exporter of animal protein, a significant reversal from its current import-reliant status.

2050: A New Equilibrium and Global Leadership

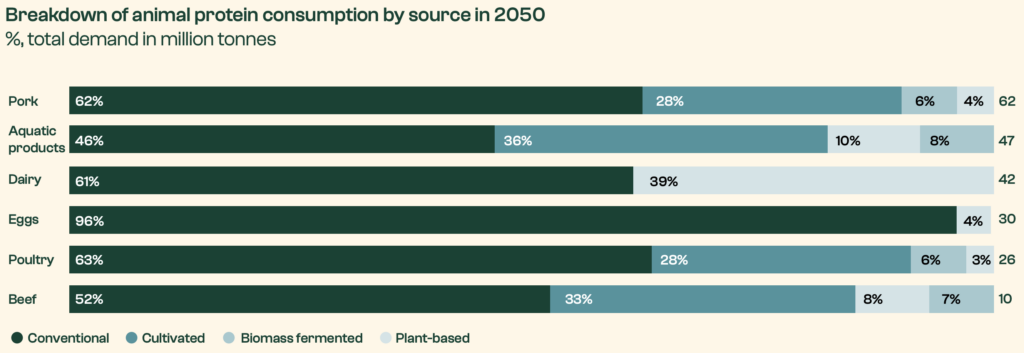

By mid-century, China’s food system is projected to be vastly transformed. A "third wave" of innovation, anticipated in the preceding decade, will make cultivated meat commercially viable, unlocking substantial segments of the animal protein market. It is estimated that alternative proteins will account for a commanding 37% to 54% of total meat and dairy consumption by 2050. While soy imports are expected to be down by 32% from a 2025 benchmark, maize imports are projected to double, driven by its dual role as a critical feed crop and a key feedstock for microbial and cultivated protein production. The demand for alternative sugar sources will also necessitate diversification, with alternative protein producers expected to adopt potatoes and sugarcane, and to explore cellulosic inputs derived from grasses and agricultural residues.

China’s substantial investments in biomanufacturing are poised to establish it as a global leader in one of the 21st century’s defining technological domains. The nation is expected to become the world’s leading producer of amino acids and other essential inputs for alternative protein synthesis. Furthermore, it will likely emerge as the dominant supplier of alternative protein infrastructure, contributing to a more stable and diverse global food system.

Global Impact and Implications: A Shifting World Order

China’s projected dominance in the future food economy carries significant implications for stakeholders worldwide. Currently, China is the primary purchaser of soy exported by Brazil, Argentina, and the United States, and a major importer of beef from Brazil, Argentina, and New Zealand. A sustained contraction in Chinese demand will not only reduce export volumes from these producer nations but also risks significant price declines and substantial losses in export revenue.

Countries heavily reliant on agricultural exports to China will be the first to experience the repercussions of this transition. To bolster their resilience, these nations will need to focus on improving productivity on existing farmland, advancing deforestation- and conversion-free commodity production, diversifying their export markets, and exercising caution regarding investments that may not yield anticipated returns.

For the global alternative protein industry, China’s industrial approach to scaling production could accelerate the timeline to price parity significantly faster than currently anticipated by many sector players. This presents both a substantial opportunity and a formidable challenge for existing producers, particularly those in Europe and the United States. Following the model established in the solar energy and EV sectors, China’s strategic intervention could dramatically reduce the cost of bioreactors and fermentation systems. While this could benefit the industry overall, it may erode the competitive advantage of early movers who have invested at higher cost bases.

Furthermore, future food industry players must be prepared for Chinese alternative protein products to enter international export markets, potentially leading to direct competition with established global brands. Navigating evolving regulatory landscapes will also be crucial, as novel food approvals and labeling requirements will significantly shape the pace of consumer adoption in different regions.

Shenggen Fan, chair professor at the China Agricultural University, commented on the strategic shift: "For years, China has been the engine of global agricultural demand, but recent climate shocks, geopolitical tensions and trade disruptions have exposed the vulnerability of that model. The new Five-Year Plan signals that Beijing has taken note, responding with characteristic resolve and embedding food security and sovereignty as a core strategic priority. Those who have watched China’s previous industrial transitions know not to underestimate what could come next." His statement underscores the historical precedent of China’s industrial policy and its potential to reshape global markets.