The Good Food Institute (GFI), a leading global think tank dedicated to advancing alternative proteins, has unveiled its highly anticipated 2026 State of the Industry Report series. This comprehensive collection of reports delves into the dynamic landscape of plant-based, fermentation-derived, and cultivated proteins, offering critical insights into market trends, consumer behavior, and policy developments throughout 2025. Despite prevailing concerns surrounding ultra-processed foods (UPFs) and a notable decline in venture capital interest, the reports reveal a resilient and growing global market for plant-based food alternatives, signaling a potential rebound for the broader alternative protein sector after a period of market correction.

The 2026 report series, which encompasses detailed analyses of plant-based, fermentation-derived, and cultivated proteins, provides an in-depth examination of the commercial, consumer, and policy environments shaping the future of food technology. The latest edition highlights the increasing consumer awareness of UPFs, the sustained and robust demand for protein sources, and the complex and often dichotomous policy approaches adopted by governments worldwide, all of which have significantly influenced the trajectory of the food tech market. The year 2025 was characterized by an expansion in sales across numerous plant-based food categories, even as many startups faced funding challenges and operational shutdowns. Simultaneously, several novel food products achieved regulatory approval, navigating a landscape often marked by efforts to restrict the labeling and sale of innovations, particularly in the cultivated meat sector. Overall, the findings suggest a positive outlook, with many industry observers anticipating a resurgence in the alternative protein sector following several years of recalibration.

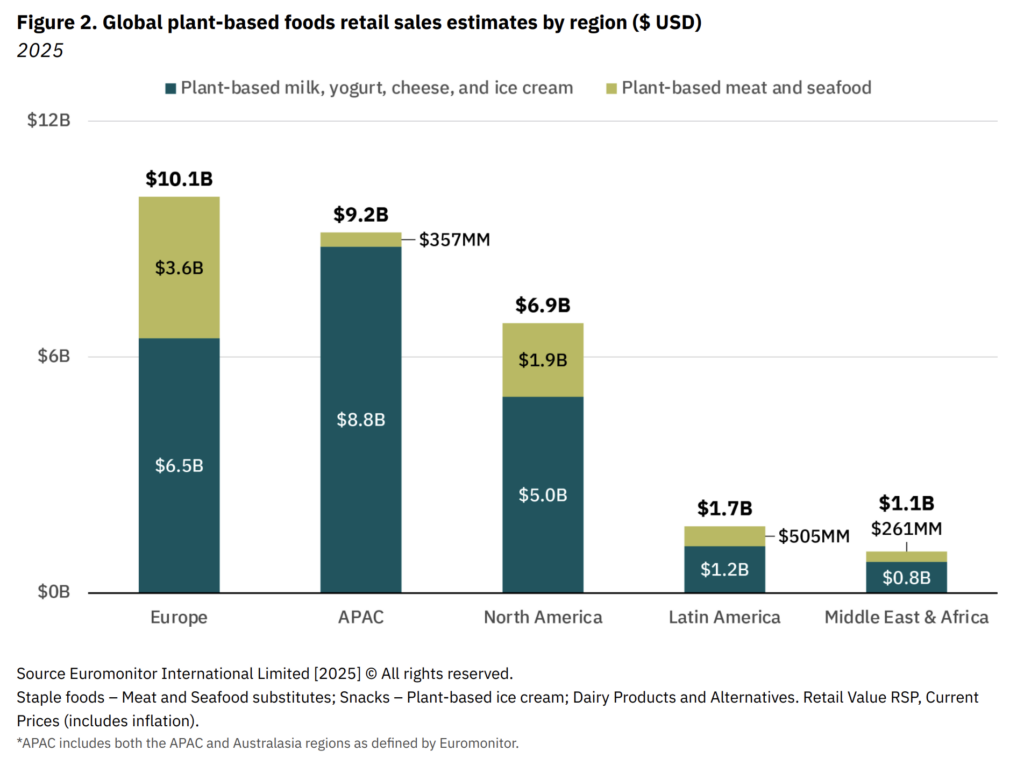

Global Plant-Based Sales Surge, Led by European Markets

Worldwide retail sales of plant-based meat, seafood, and dairy products reached an impressive $28.9 billion in 2025, representing a 3% increase from the previous year, even after accounting for inflation. This growth underscores a continuing consumer shift towards plant-forward diets.

Non-dairy products continue to dominate the plant-based market, accounting for $22.7 billion, or 78.5% of total plant-based sales. While volume sales for non-dairy products remained flat, dollar sales saw a modest 2% increase. Within this segment, milk alternatives emerged as the leading category, generating $18.2 billion in sales.

Plant-based meat, however, demonstrated even more significant growth in 2025. Retail sales in this category are estimated at $6.6 billion, an 8% year-on-year increase, and a 4% rise when adjusted for inflation. The growth in volume purchases, up by 3%, suggests that increased consumer adoption was a primary driver of overall sales figures.

The robust performance of plant-based meat alternatives was largely propelled by a surge in demand within Europe. The continent solidified its position as the largest global market for plant-based foods, with total sales of meat and dairy alternatives reaching $10.1 billion. The Asia-Pacific region followed, with sales of $9.2 billion, and North America recorded $6.9 billion in plant-based food sales. This geographical distribution highlights the diverse adoption rates and market maturity across different global regions.

US Plant-Based Market Faces Headwinds, Yet Shows Pockets of Growth

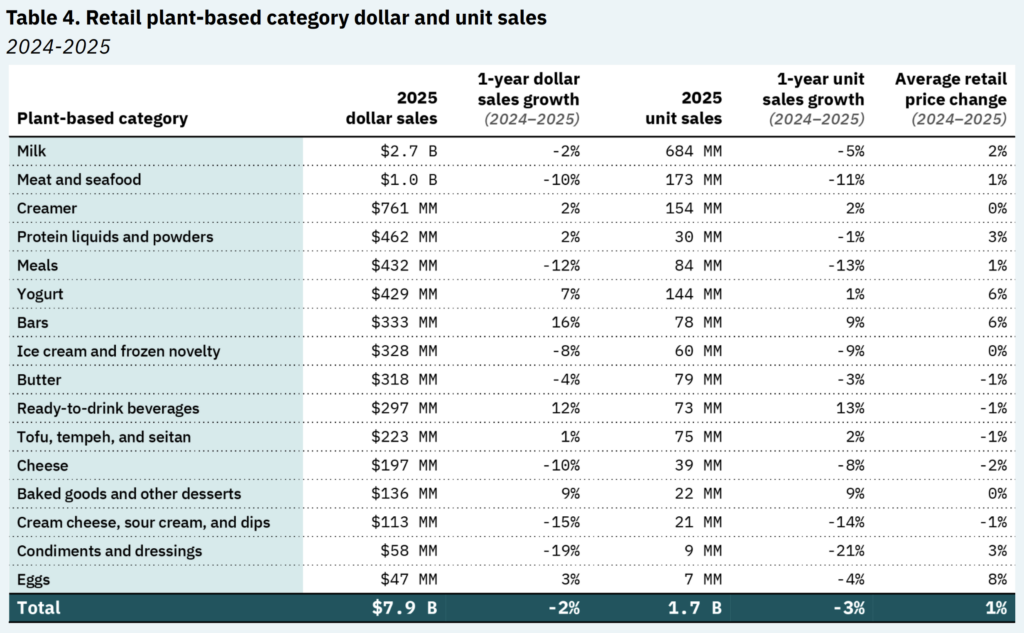

In contrast to the global trend, the United States market for plant-based foods experienced a slight contraction in 2025. Overall sales were recorded at $7.9 billion, a 2% decrease from the prior year, according to data from SPINS. This slowdown reflects a complex interplay of factors, including evolving consumer preferences and increased competition.

Plant-based meat and seafood categories continued to face challenges, with dollar sales declining by 10% to $1 billion and unit sales falling by 11%. Non-dairy milk, while remaining the largest category with $2.5 billion in dollar sales, also saw a 2% decline.

Despite these broader market declines, specific segments within the US plant-based sector demonstrated resilience and growth in 2025. Soy milk and coconut milk experienced notable increases in sales, up by 4% and 27% respectively. In the plant-based meat category, chunks, shreds, and strips saw an impressive 8% rise in unit sales, indicating a consumer preference for these versatile formats.

Other categories that performed well in terms of retail sales included bars (up 16%), ready-to-drink beverages (up 12%), baked goods (up 9%), yogurts (up 7%), eggs (up 3%), and creamers and protein powders (each up 2%). Tofu, tempeh, and seitan also witnessed a modest 1% increase in purchases.

The foodservice sector presented a mixed picture. Total broadline distributor sales of plant-based proteins, encompassing meat alternatives, tofu, tempeh, and veggie burgers, reached $291 million in 2025, marking a 7% decrease in dollar sales. However, certain plant-based meat formats, along with milk alternatives ($288 million in sales, up 14%) and creamers ($189 million in sales, up 4%), experienced an uptick in demand within the foodservice channel. This suggests that while overall plant-based protein sales in foodservice may have declined, specific product types are gaining traction.

Shifting Price Dynamics and Consumer Reach in the US Plant-Based Market

The year 2025 presented a complex pricing environment for plant-based foods in the US, largely influenced by broader inflationary pressures. Despite these challenges, the price of plant-based meat saw a marginal increase of only 1%. Several plant-based products, including butter, ready-to-drink beverages, cheese, tofu, tempeh, and sour cream and dips, actually became more affordable, suggesting improved production efficiencies and competitive pricing strategies.

However, plant-based milk prices rose by 2% in 2025, reversing a previous year’s decline. Plant-based eggs experienced the most significant price increases, up by 8%, followed by yogurts and bars, each rising by 6%. These fluctuations highlight the varied cost structures and market dynamics within different plant-based product categories.

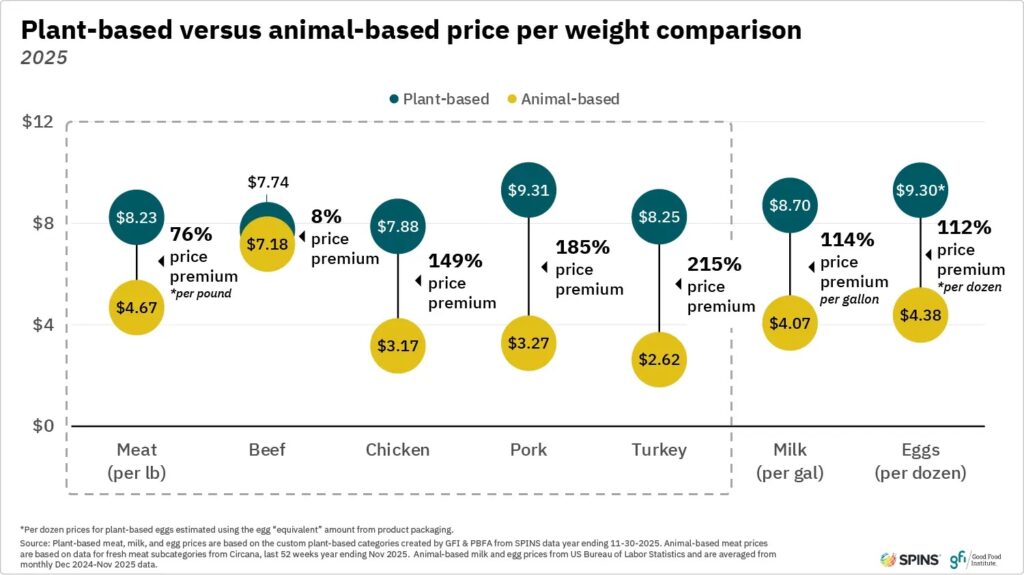

A positive development for the industry was the narrowing price premium of plant-based meat alternatives compared to their conventional counterparts. In 2025, plant-based meat carried an average price premium of 76%, a decrease from 82% in 2024. This convergence is particularly evident in the plant-based beef segment, which now carries only an 8% premium over conventional beef, a trend directly attributable to the record-high prices of beef in the US during 2025. While the price gaps for plant-based chicken and pork remained relatively stable, plant-based milk remained significantly more expensive than cow’s milk, with a 114% premium, and vegan eggs were 112% costlier than their animal-derived equivalents.

The penetration of plant-based products into US households also contracted in 2025. Overall, 60% of US households purchased at least one plant-based SKU, and 78% of these households made repeat purchases. However, penetration rates declined for both milk and meat alternatives, standing at 38% and 11% respectively. Repeat purchase rates remained relatively strong, at 75% for milk alternatives and 62% for meat alternatives, indicating that consumers who do purchase these products tend to remain loyal. Despite these figures, vegan meat and seafood products still represent a small fraction, just 1%, of total US retail meat sales, a stark contrast to the 13% market share held by non-dairy alternatives in the milk category.

Venture Capital Funding Dips to Seven-Year Low Amidst Soaring Public Investment

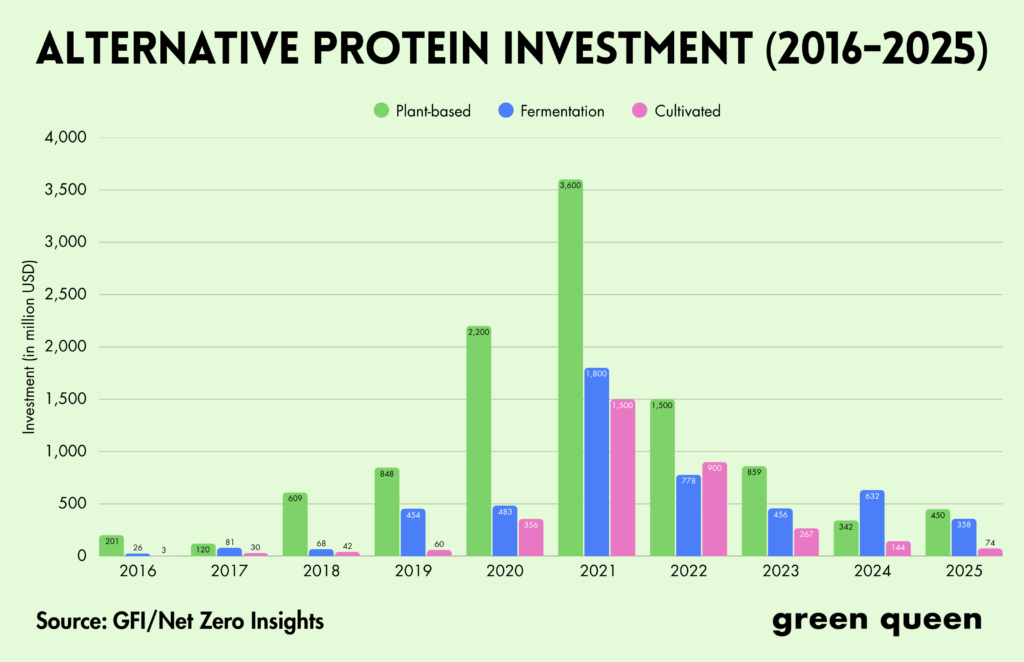

The alternative protein sector experienced a significant downturn in venture capital (VC) funding in 2025, reaching its lowest point in seven years. According to GFI’s analysis of Net Zero Insights data, total funding for the sector fell by 20% to $881 million, marking the first time it has dipped below the $1 billion threshold since 2018. This decline reflects a broader trend of reduced VC investment in growth-stage companies across various sectors, driven by economic uncertainties and a recalibration of investment strategies.

Investment in fermentation companies saw a substantial decline of 43.5% from its 2024 peak, totalling $357 million. The cultivated meat sector fared even worse, attracting only $74 million, nearly half of the funding secured in the previous year.

The plant-based segment was the sole category to surpass its 2024 total, with investments reaching $450 million, a 31.5% increase. However, this growth was significantly bolstered by a $100 million debt financing round from Beyond Meat. Excluding this substantial debt facility, the plant-based category would have seen a more modest 2% increase in funding.

In stark contrast to the private investment landscape, public investment in the alternative protein ecosystem witnessed remarkable growth. In 2021, collective public funding for the sector totaled $700 million. By 2025, this figure had surged to $2.5 billion, representing a more than fourfold increase over four years. This substantial rise was primarily driven by significant investments from China and the European Union, underscoring a growing governmental commitment to fostering the development of sustainable protein sources. Furthermore, the number of countries actively working to advance this industry has doubled, from 16 to 33, indicating a global recognition of its strategic importance.

Consolidation and Restructuring Mark the Alternative Protein Landscape

The alternative protein sector continued to experience a high degree of consolidation and restructuring in 2025. Analysis indicates that since September 2024, over 70 alternative protein businesses have undergone mergers, acquisitions, buyouts, insolvency proceedings, or have ceased operations. GFI’s reports attribute this wave of consolidation directly to the sector’s persistent funding challenges. In 2025 alone, 19 plant-based companies were acquired, while several others suspended or terminated operations due to difficulties in securing follow-on financing.

The cultivated meat sector was particularly affected by these financial pressures. Unsuccessful fundraising efforts and ongoing financial struggles led to the closure of prominent startups such as Meatable and Believer Meats. To navigate these challenges and foster innovation, several companies pursued mergers and acquisitions. Nexture Bio acquired Matrix FT, Gourmey merged with Vital Meat to form Parima, and Fork & Good acquired Orbillion Bio, demonstrating a trend towards industry consolidation to leverage external technologies and enhance competitive positioning.

While the fermentation category did not experience the same pace of consolidation, it was not immune to setbacks. Several high-profile closures and restructurings, including those of Bolder Foods, Arkeon, NovoNutrients, and Planetarians, challenged existing assumptions regarding timelines, scale-up pathways, and inherent risks within the industry. Libre Foods was acquired by Planetary, and Meati Foods was rescued from the brink of collapse through a $4 million buyout. These events underscore the intense competitive environment and the capital-intensive nature of developing and scaling novel protein technologies.

Regulatory Milestones Achieved Amidst Growing Legislative Hurdles

The year 2025 marked a significant period for cultivated meat regulation, with six companies achieving regulatory approval to sell their products for human or pet food consumption. These approvals were granted to Vow (Australia), Wildtype, Mission Barns, Believer Meats (all US), Friends & Family Pet Food Company, and Parima (both Singapore). These milestones represent crucial steps towards the commercialization of cultivated meat on a broader scale.

Furthermore, numerous fermentation-derived ingredients successfully navigated regulatory pathways. In the United States, ten precision- and biomass-fermented products received "no questions" letters from the Food and Drug Administration (FDA), indicating that the agency had no objections to their use. Several other companies successfully self-determined their ingredients as Generally Recognized as Safe (GRAS).

However, these regulatory achievements were juxtaposed with a series of legislative challenges faced by the alternative protein sector. Notably, the self-affirmed GRAS pathway is slated for elimination under a directive from Health Secretary Robert F. Kennedy Jr. This proposed change is expected to significantly increase the time and financial resources required for companies to obtain regulatory approval for new ingredients.

In a concerning trend for the cultivated meat industry, several US states followed the lead of Florida and Alabama in banning the sale of cultivated meat. In 2025, Mississippi, Montana, Indiana, Nebraska, and Texas enacted such bans. South Dakota became the latest state to join this cohort last month. These legislative actions create a fragmented regulatory landscape and pose significant barriers to market entry and expansion for cultivated meat producers in the United States.

Across the Atlantic, the European Union reached an agreement last month to prohibit companies from using 31 meat-related terms on the packaging labels of plant-based and cultivated protein products. This decision, following months of intense debate in 2025, aims to prevent consumer confusion and maintain the integrity of traditional meat product terminology. While intended to clarify labeling, it presents a challenge for companies seeking to leverage familiar language to market their innovative protein alternatives.

The authors of GFI’s policy report emphasized the need for continued and dedicated funding to enhance consumer appeal and availability of new protein sources. They stated, "Though broader biotechnology development programmes show promise for creating the infrastructure and workforce needed for a more resilient food system, dedicated funding to increase consumer appeal and availability of new protein sources is necessary to build a futureproof food system." This underscores the critical role of both public and private investment in driving innovation and market adoption within the alternative protein sector. The interplay between technological advancements, consumer acceptance, and evolving regulatory frameworks will continue to shape the future of food.